CFPB warns providers to stop junk fees on international money transfers

So, will “fee-free” and “no fee” advertising disappear tomorrow?

In 2018, the United Kingdom first allowed payment companies to gain direct access to its payments systems. Several other countries, in the midst of their own payments modernization initiatives, are following suit. That’s why comments earlier this year from Governor Lael Brainard of the U.S. Federal Reserve caught my attention:

"Given the growing role of nonbank technology players in payments, a review of the nation’s oversight framework for retail payment systems could be helpful to identify important gaps.”

She’s right. Payment companies, like the money transfer applications on your phone, offer critical services to consumers yet are often caught in regulatory limbo in the United States.

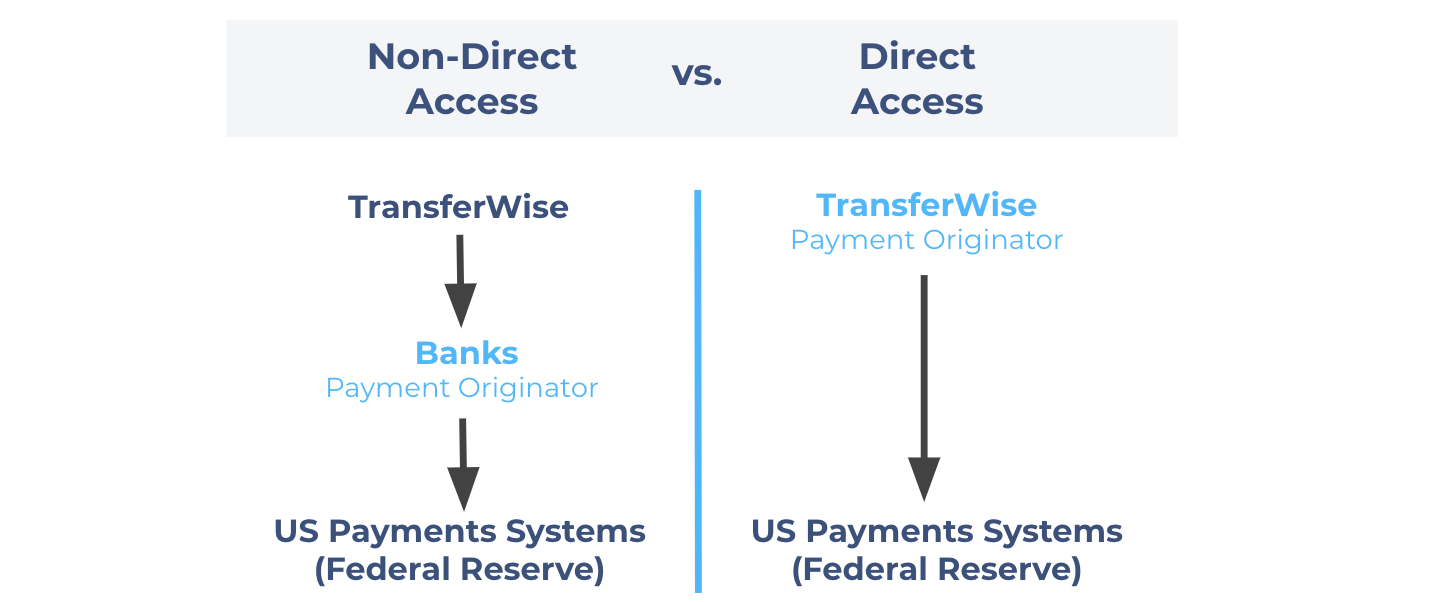

Today, payment companies typically obtain state money transmission licenses, but those licenses do not permit direct participation in the nation’s payments systems (FedWire, FedACH, and, eventually FedNow). Instead, because of outdated regulations, payment companies must rely on banks as a costly middleman to originate and settle payments on their behalf. While FedACH payments only cost .35 cents to send directly, it often costs payment companies 30 cents or more per transaction through a bank partner. Consumers eat the difference with higher costs.

The only way to gain direct payments access is to become a bank. Problem is, a traditional bank license doesn’t make sense for a payment company that does not lend or take deposits. A bank license might require a payments company to change its business model, possibly adding more friction and costs for customers, to make the decision economically feasible. Regulations shouldn’t have that impact.

Whether at the state or national level, there is no license that provides direct payment participation. This regulatory gap means licensed and regulated payment companies cannot access the payments infrastructure despite this being their core expertise.

That's like telling a heart specialist that they can’t use a stethoscope in private practice; stethoscopes can only be used in big hospitals.

This is a problem other countries have recognized more quickly. As Governor Brainard wisely continued,

“A good place to start may be contrasting the US oversight framework for retail payment systems with other jurisdictions.”

Canada offers a current example. They’re in the process of creating a Retail Payments Oversight Framework that would form a national licensing and supervisory regime for payment companies, and subsequently allow limited membership and direct participation in the forthcoming faster payments system.

Canada is following the lead of the United Kingdom, which, as part of the European Union, created a modern payments licensing regime over the last decade, and offers direct payments participation to e-money and payment institutions. European consumers are already benefiting from lower costs and better services. That’s why Singapore and Australia, like Canada, are similarly following suit.

Even international bodies like the World Bank and others have called for increased access to payments systems to improve the marketplace and boost financial access and inclusion. Earlier this month, the G20’s Financial Stability Board, which is chaired by Federal Reserve Vice Chair Randy Quarles, recommended that countries review and consider expanding domestic payments access for non-banks in its cross-border payments report.

Under the current regulatory regime, payment companies rely on bank partners - often competitors - to access payment rails. That ultimately results in added costs to the customer and concentrates risk in a handful of the largest banks who process most payments.

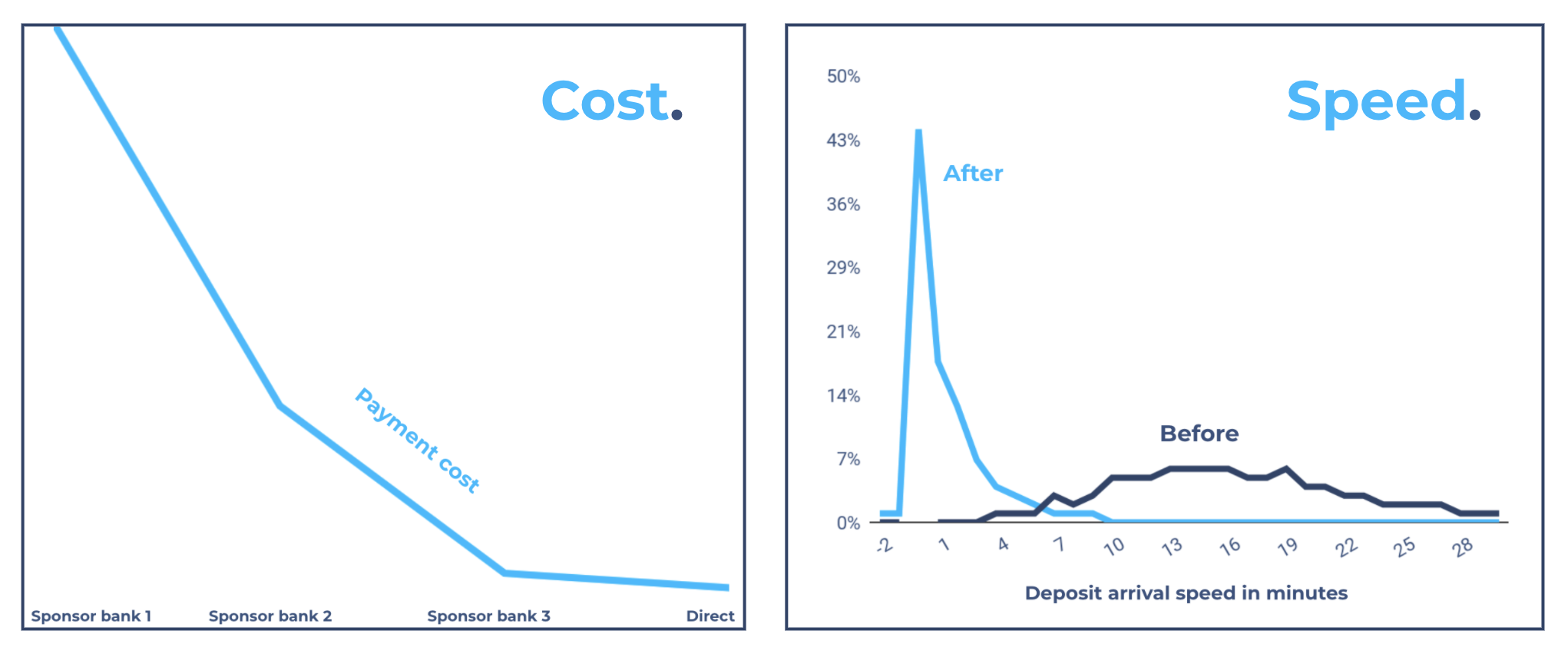

A modern regulatory framework with expanded participation in the payments system would benefit consumers with lower costs and improved services through increased innovation and competition. For example, our UK customers pay half the fees of our US customers on average. Why? Because in 2018, Wise gained direct access to the UK’s payments system and passed those savings directly to our customers.

This initiative would also boost financial stability by diversifying risks and eliminating single points of failure within the payments system, while providing regulators with oversight and visibility into payment operations.

Governor Brainard started it earlier this year, and Acting Comptroller of the Currency Brian Brooks turned up the volume in recent months with his advocacy for a national payments charter that could lead to Fed access.

The United States is behind. We hope all parties - including the OCC, Federal Reserve, Congress, and the State Bank Supervisors - come together to jointly build a modern retail payments regulatory framework that allows the private sector to increase competition, reduce costs, and improve customer services.

The Fed should have buy-in to offer access to payments infrastructure. Congress should have buy-in to provide bipartisan support and ensure long-term success. And, the States should have buy-in too, as they offer expertise and historical perspective on money transmission regulation.

The United States needs to modernize its payments regulatory framework. Let’s find a way to make sure the politics don’t get in the way of good public policy.

*Please see terms of use and product availability for your region or visit Wise fees and pricing for the most up to date pricing and fee information.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Wise Payments Limited or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional.

We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

So, will “fee-free” and “no fee” advertising disappear tomorrow?

There should be nothing to hide Sending money abroad is a big deal for many Brazilians living international lives. You might be supporting your family,...

“Junk fees” were certainly a buzz word of 2023, as the Biden Administration announced a crackdown across industries to protect American consumers. The White...

In a year, US military service members spent more than $455 million on foreign exchange fees. Of that, $301 million was lost in hidden fees.

Wise was founded by immigrants, built by immigrants, and is used by immigrants.

£187 billion! That’s how much people and businesses lost to hidden fees in a single year.